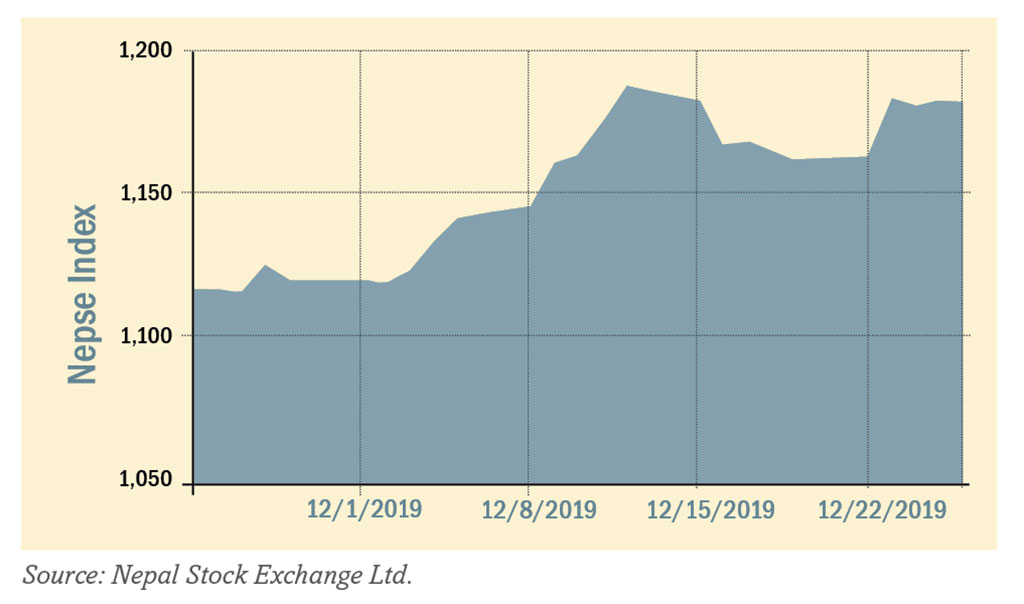

During the review period of May 22 to June 19, the Nepal Stock Exchange (NEPSE) index plunged by 110.95 points (-8.30%) and closed at 1,226.18 points. The secondary market, yet again witnessed a turbulent month; the index started on a free fall and showed some recovery to reach 1,336.39 points. Since the market couldn’t withstand the selling pressure, the market is on a declining spree, dropping below the psychological level of 1,300 points and closing at 1,226.18 points. Furthermore, the total trading volume during the period decreased substantially by 30.42% and stood at Rs 6.53 billion.

Beside the impact of tight liquidity in the banking system, the decline is mainly on account ofannouncement in national budget that increased the tax burden of the individual investors by increasing the Capital Gain Tax (CGT) on shares to 7.5% from the previous 5%. Further the notice published by Inland Revenue Department to calculate the CGT on bonus share and right share by considering the paid-up value as purchase price fuelled the bearish movement of the NEPSE. However, the notice was withdrawn by IRD as the investor group protested and decided not to trade.

During the review period, all the sub-indices landed in the red zone except for Manufacturing and Processing.

The Insurance sub-index (-10.03%) led the pack of losers with the decrease in share value of Rastriya Beema Company (-Rs 1,401), Prabhu Insurance (-Rs 265), National Life Insurance (-Rs 169), and Everest Insurance (-Rs 163). Similarly, Commercial Bank sub-index (-9.35%) was second in line with the slump in share value of NMB Bank (-Rs 110), Everest Bank (-Rs 61) and Nabil Bank (-Rs 58). Likewise, Microfinance sub-index (-7.70%) followed the suit with decrease in share value of key microfinance companies such as Mirmire Microfinance (-Rs 1,465), RSDC Microfinance. (-Rs 311) and Naya Nepal Microfinance (-Rs 251).

The Development Bank sub-index (-7.38%) went down with the decrease in the share value of Gandaki Development Bank (-Rs 63), Kabeli Development Bank (-Rs 48) and Muktinath Development Bank (-Rs 32). This was followed by Hydropower sub-index (-7.18%); top losers in this index were Chilime Hydropower (-Rs 71), Butwal Power (-Rs 36), Sanima Mai Hydropower (-Rs 34). Likewise, the others sub-index (-5.27%) shed value with the decrease in the share value of Citizen Investment Trust (-Rs 208) and Nepal Telecom (-Rs 35). Likewise, Finance sub-index (-5.06%) also decreased as the share value of Pokhara Finance Ltd. (-Rs 22) and ICFC Finance Limited (-Rs 15) decreased. The only gainer, Manufacturing & Processing (+ 1.26%) rose with the increase in the share value of Unilever Nepal Limited (+Rs 1,539).

News Highlights

News Highlights

Securities Board of Nepal (SEBON) has amended its provision on application for Initial Public Offering (IPO) and Further Public Offering (FPO) issue. Accordingly, the issuing company can now decide the maximum units of shares to be applied by the interested investors in the IPO and FPO allowing the investors to apply for as many shares as mentioned as maximum limit in the offer letter published by the company. Previously, the investors could apply for maximum 0.5% of the total IPO and/or FPO issue.

On June 5 no shares were traded on the floor of NEPSE due to investors protest against the IRD’s circular on revising the method of CGT by fixing Rs 100 as the base price of per unit of bonus and right share. The new method to calculate CGT is currently put on hold. SEBON, NEPSE and CDS and Clearing Centre have suggested the Government to calculate the CGT on weighted average price.

The most awaited online trading system will be implemented fully only after Dashain at the earliest. Earlier SEBON had announced that the full-fledged implementation will take place by mid-July. The full-fledged implementation will take place only after the completion of User Acceptance Testing (UAT) and approval of the same from SEBON.

In the public issue front, NMB Bank Limited issued FPO of total 11.4 million shares worth Rs 3.8 billion at Rs 333 per share. After capitalisation of all FPO shares its paid-up capital will increase to Rs 7.60 billion from Rs 6.46 billion, which will help in meeting the capital requirement of Rs 8 billion stipulated by the Central Bank. The issue was assigned IPO grade 3 by ICRA Nepal indicating average fundamentals. Since the issue is not fully subscribed the FPO issue has been extended up to July 12. Meanwhile, SEBON has approved FPO worth Rs 4.95 billion of Nepal Bank Limited. The issue price per unit share is Rs 280. This FPO issue will raise the company’s capital from Rs 8.04 billion to Rs 9.81 billion. After the issuance, the stake of government in Nepal Bank Limited will be maintained at 51% which is currently 62%.

SEBON has approved the IPO of Upper Tamakoshi Hydropower Limited (UTHL) worth Rs 2.65 billion at Rs 100 per unit share. After the issue, the company’s capital will reach Rs 10.59 billion from Rs 7.94 billion. Out of the total issue of 26.5 million unit shares, 10.59 million unit shares will be issued for local people and remaining 15.89 million unit shares will be issued for general public. ICRA Nepal has assigned IPO Grade 4 indicating below-average fundamentals.

Outlook

Outlook

The budget for the FY 2018/19 has made it mandatory to list private companies from the real sector with investment above Rs 1 billion in the secondary market. Since almost 85% of listed companies are from the financial sector, the move can attract real sector companies into the market and further deepen the market. On a positive note, SEBON has already granted approval to Shivam Cement to issue public shares at premium, the response of general investors over the upcoming IPO would play a pivotal role to attract other real sector companies into the market. Meanwhile, as the government expedites capital expenditure in the last quarter of the fiscal year, liquidity in the banking system is expected to ease, which could bring favourable impact on the secondary market. Further, as the monetary policy 2018-19 is expected to unveil soon, the provisions could impact the future course of the market.

This is an analysis from beed invest ltd. No expressed or implied warrant is made for usefulness or completeness of this information and no liability will be accepted for consequences of actions taken on the basis of this analysis.