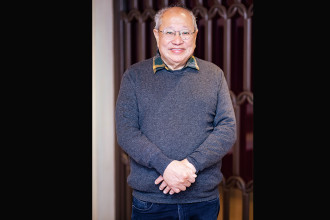

Sachindra Dhungana

Deputy General Manager, NIBL Ace Capital

With the mutual fund market gradually gaining traction in Nepal, Business 360 spoke to Sachindra Dhungana, Deputy General Manager, NIBL Ace Capital, to get a better understanding of how the mutual fund market has developed in Nepal and its investment benefits. Dhungana is a Qualified Chartered Accountant from The Institute of Chartered Accounts of Nepal (ICAN) and also holds a diploma in International Financial Reporting Standards (IFRS) from ACCA. It has been more than 10 years that he has been working in the field of auditing, accounting, consultancy, advisory and investment banking. He also has pioneer experience in mutual fund management, assets management and corporate advisory services in the Nepali capital market. Dhungana was previously associated as with SR Pandey & Company Chartered Accountants, NIBL Capital Markets and Nabil Investment Banking. Excerpts of an interview:How has the mutual funds market evolved in Nepal and how do you see its growth in the coming years?

Mutual fund is a professionally managed investment fund that pools money from many investors to purchase securities. In this era of globalisation and competition, success of an industry is determined by the market performance of its stock. In the initial days, the growth of mutual funds in Nepal was very slow and it took a really long time to evolve into modern-day mutual funds. The first mutual fund introduced in Nepal was the NCM mutual fund by Nepal Industrial Corporation in 1993. It had a maturity period of 10 years and hence closed by the end of fiscal year 2000/2001 AD. The Securities Board of Nepal (SEBON) officially issued directives known as the ‘Mutual Fund Regulation, 2067 in 2067 BS. In Nepal, there are currently 37 mutual funds out of which 31 are close-ended mutual funds and six are open-ended mutual funds. Mutual funds are still in a growing phase in Nepal where multiple new mutual funds are introduced every year. Such kind of growth has helped broaden the relatively new capital market of the country and has helped small-time investors with secured and high returns. It has potential for even higher growth as it opens the door of opportunity to anyone with any amount of investment capital but no knowledge or resources and also because it is generally considered that mutual funds fare well in small markets such as Nepal.We were pretty late in introducing the mutual fund concept in the country when compared to other countries. Your thoughts.

The concept of mutual funds has been around for a long time with the Dutch being regarded as the early creators of the first type of mutual fund believing that the diversification would appeal to investors with low capital. Mutual funds really began to capture the imagination of investors around the 1980’s and 90’s when it hit record highs with incredible returns for many American investors and have been mainstream ever since. Comparatively, the history of mutual funds in Nepal began with the introduction of ‘NCM Mutual Fund 2050’ in 1993. The Mutual Fund Regulation 2010 has played an important role in the development of mutual funds as there has been significant progress after its implementation. Comparing the ratio of mutual funds, it can be seen that there is less attraction of investors towards mutual funds in the Nepali market. However, it is seen that the proportion of investment in mutual funds has increased in recent days. The success of any mutual fund, a popular means of investment, depends on how effectively any merchant banking facility has been able to understand the level of influence of these factors on the decision of investors to invest in mutual funds. With the passage of time many opportunities are available to investors to invest their money in different investment channels. One such channel is to invest in mutual funds along with effective financial management. Mutual funds have seen a tremendous growth in the last few years. This is the result of combined efforts of financial institutions and fund managers who come to one’s rescue by educating investors and making them aware of the mutual fund schemes through different modes of promotion.What are the major areas of investment that NIBL Ace Capital focuses on?

The major areas of investment that NIBL Ace Capital focuses on are:- Listed securities that are registered with SEBON

- Bond and Debentures

- Securities called for public offering (IPO, FPO, right shares)

- Money Market Instruments

- Bank Deposits

- Others sectors/areas prescribed by SEBON

Mutual funds are considered to be important to minimise risks associated with investments. Could you please elaborate on how risks are minimised for the investor?

For investors with limited time to spend watching the ups and downs of the markets, mutual funds offer a good alternative due to the following reasons:- Mutual funds offer diversification or access to a wider variety of investments than an individual investor could afford to buy.

- Mutual funds are supervised by experienced fund supervisors who have vast experience regarding technical and functional overview of the financial markets.

- The investments made in mutual funds by the fund supervisors are done through extensive research and market analysis.

- Monthly contributions in the case of SIP’s (Systematic Investment Plan) help the investor’s assets grow.

- Mutual funds are more liquid because they tend to be less volatile.

- Investors get professional investment management services through mutual funds.

Low returns on mutual funds are touted as the main reason for a lukewarm response from the public. Will this change?

Well, it is not true that mutual funds have low return; it is just a misconception in people’s mind. We will have to look at the data for this; currently existing mutual funds that have completed more than five years and those mutual funds that have already matured in Nepal have provided an average annual return of 15.76% including both capital gain yield and dividend yield. The average total yield of these funds is more than 85%. Additionally, if we simply consider mutual funds that have already reached maturity, they have given their unit investors an alluring average annual return of 24.12%. However, the average annual return in the fixed deposit rates provided by banks and financial institutions (Class A, B and C) in the past seven years (2015-2022) is 8.57% and the average annual return from the mutual funds traded in Nepal Stock Exchange is 15.76%. This data justifies that investment in mutual funds beats average fixed deposit rates. Moreover, being professionally managed, the fund supervisors take calculated risks backed by appropriate research while investing the fund pooled from the investors. Thus, it won’t be wrong to say that mutual funds provide comparatively better returns and hopefully will gain popularity in the market with the passage of time.Mutual fund trading in the stock market is quite insignificant. What could be the reason?

I think discouraging the trading of mutual funds in the stock market could be a solution, because mutual funds are usually for longer period of time and trading in stock market is for short term. People trading in the stock market expect returns and high profits in shorter time span, but what they are not aware of is the higher the return you expect, the higher the risk you take. Hence, we could encourage a Systematic Investment Plan (SIP), more popularly known as SIP which is a facility offered by mutual funds to the investors to invest in a disciplined manner. SIP facility allows an investor to invest a fixed amount of money at pre-defined intervals in the selected mutual fund scheme. The fixed amount of money can be as low as Rs 1,000, while the pre-defined SIP intervals can be on a monthly/quarterly/semi-annually or annual basis. By taking the SIP route to investments, the investor invests in a time-bound manner without worrying about the market dynamics and stands to benefit in the long-term due to average costing and power of compounding. With this scheme I believe that the misconceptions about mutual funds will lessen and also people might be interested in mutual funds and their schemes even in the stock market after understanding its concept fully in the future.Are there any government policies you would like introduced or amended for the mutual fund market to grow?

In order to get a perspective on what policies can be introduced or amended for the mutual fund market to grow, we need to first get a bigger picture of what is happening in the global scenario. The main goal for investing in any mutual fund for an individual is to see their investments grow at a higher rate compared to fixed deposits offered by the banks. In order to attract more individuals to mutual funds there has to be a tax benefit associated with it. In India, capital gains on mutual funds are not taxable. Similarly, the net income of the fund is also not taxable. The unit holders in India also do not have to pay Dividend Distribution Tax (DDT) unlike in Nepal. Changes in policies regarding tax benefit would definitely boost the mutual fund industry in Nepal. Secondly, there are limited avenues where fund managers can invest in the mutual fund industry in Nepal. Introduction of new money market instruments such as forwards, futures, options and swaps; commonly known as derivatives will play a pivotal role in boosting the mutual fund market. This will provide fund managers a wider range of investment avenues through which they can reduce their risks. In India, the Securities and Exchange Board of India (SEBI) permits mutual funds to use derivatives for hedging purposes. The mutual fund can hedge its equity investments using derivatives. Besides this, derivatives are also used for arbitrage strategies by mutual funds. In a nutshell, the mutual fund industry in Nepal has reached its maturity but there is still room for more growth. In order to attract more individual investors, tax benefits associated with mutual funds have to be implemented. For the overall growth of the mutual fund industry as well as the Nepali capital markets, introduction of new money market instruments is also imperative.For the layman, could you explain the difference between close-ended and open-ended funds?

Mutual funds in Nepal are differentiated as two types, based on their investment structure, i.e. whether they are open-ended funds or close-ended funds. The difference between open-ended and close-ended funds is a function of investment flexibility and the ease with which they can or cannot be bought or sold. An open-ended mutual fund refers to a mutual fund that issues directly to investors and redeems them, based on the fund’s net asset value (NAV), which is computed daily. Open-ended mutual fund has no fixed maturity date and is perpetual in nature. close-ended fund is a type of mutual fund whose shares can be purchased and sold on a stock exchange. It is called close-ended because it has a fixed number of shares outstanding and no new shares will be issued by the fund after its initial public offering. Close-ended funds also have a fixed maturity date. People often ask which is better. We believe an open-ended fund is a much better option as it allows you to invest anytime you wish based on the surpluses you have in hand and that they are highly liquid as they can be redeemed anytime. Open-ended funds are also a better option as you can start investments with a small amount and can also invest through SIPs for the long term to meet your financial goals. These are the key differences between open-ended and close-ended funds which gives open-ended mutual funds an edge over close-ended mutual funds.Are there any new offerings from NIBL Ace Capital in the near future?

NIBL Ace Capital is in the process of launching a new mutual fund scheme named ‘NIBL Stable Fund’. For this purpose, we have already submitted the application to SEBON on September 23, 2022. This is a close-ended mutual fund scheme where we are planning to issue 100 million units at a par value of Rs 10. Hence, the total issue amounts to Rs 1 billion. On September 4 last year, NIBL Ace Capital received the Fund Manager Licence for Specialised Investment Fund from SEBON. This licence has not only opened the doors for prospective investors but also for investors who are seeking to make investments in unlisted companies and projects where detailed investment analysis is required in pre-investment phase and efficient portfolio management in post-investment phase with proper exit strategy. In a nutshell, the business dynamics are no longer limited to IPO-related merchant banking services, but the services have widened from consultancy to investment funding to the institutions project assessment to project management. Private Equity and Venture capital (PEVC) is a newly introduced alternative financing model in Nepal. Looking at the current trend PEVC could gain importance in Nepal. SIF regulations are beginning and one cannot expect them to be perfect already. Harmonisation of different Acts and regulations (like Industrial Enterprise Act, Income Tax Act, FITTA, etc) in line with SIF regulations are needed. SIF regulations itself need to clarify a lot of issues. SEBON should be able to function as a facilitator on approvals, regulatory compliance, tax matters and provide one-point solution in bringing investment, creating fund and making investments. We have smaller funds at present, we can attract sector agnostic and sector specific bigger size funds by simplifying the process. Growth of PEVC industry can create a significant impact on Nepal’s economy by availing collateral free risk capital making PEVC funds ‘an impact fund’ in the real sense. READ ALSO:- ‘Govt should prioritise climate, environmental risks in energy projects’

- ‘The office furniture market has gone through a lot of transformation’

- ‘Our business in the entire Asian market has been immense and we are leaders in our segment’

- ‘If you look at the Doing Good Index there are four sets of indicators’

- ‘I was recently at a banking and finance conference in Kathmandu and it was an eye-opener for me’

Published Date: March 2, 2023, 12:00 am

Post Comment

E-Magazine

RELATED Face 2 Face